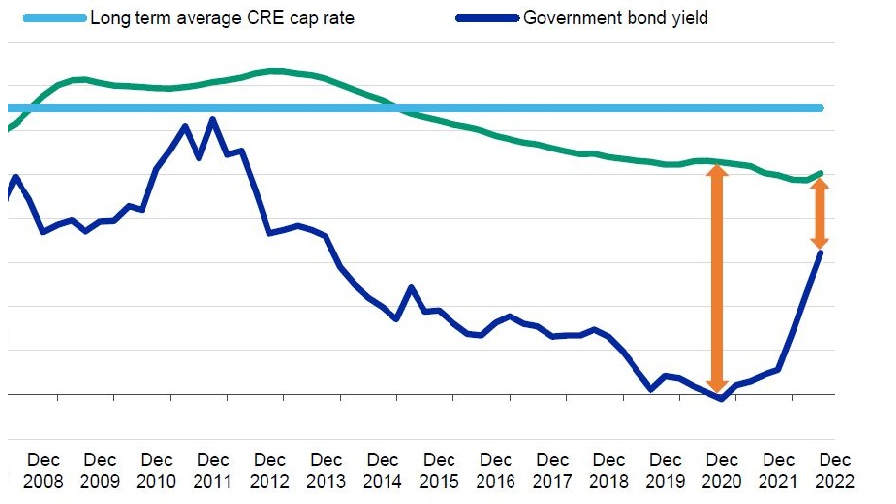

Reviewing their debt financing strategy is the highest priority for many investors, as interest rates continue to rise and values start to fall.

Premium subscriber content – please log in to read more or take a free trial.

Reviewing their debt financing strategy is the highest priority for many investors, as interest rates continue to rise and values start to fall.

CDC Investissement Immobilier, the real estate asset management subsidiary of French financial institution Caisse des Dépôts, has inked a strategic partnership with Covivio in Germany.