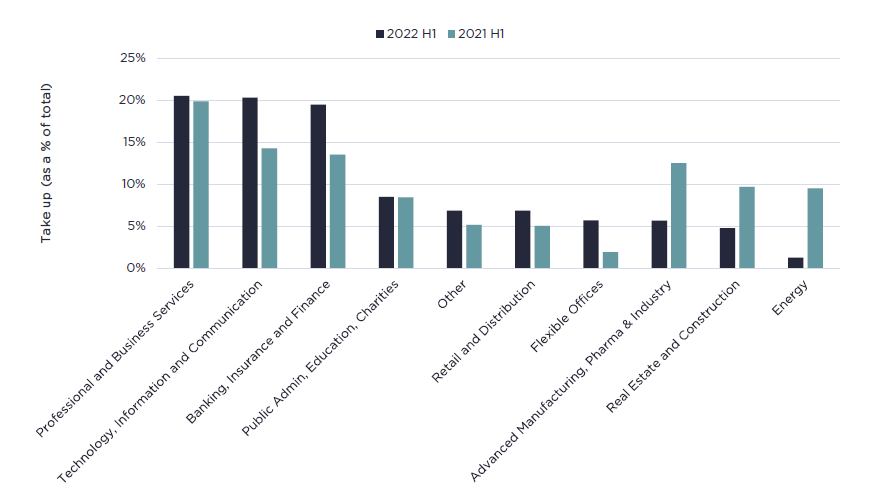

According to new research from Savills, take up in the European office market in H1 2022 reached 4.3 million m2, 11% above the five year H1 average.

Premium subscriber content – please log in to read more or take a free trial.

According to new research from Savills, take up in the European office market in H1 2022 reached 4.3 million m2, 11% above the five year H1 average.

Portuguese real estate investor and developer Bondstone is investing around €70 mln in a residential development in Belas Clube de Campo, municipality of Sintra, Portugal.