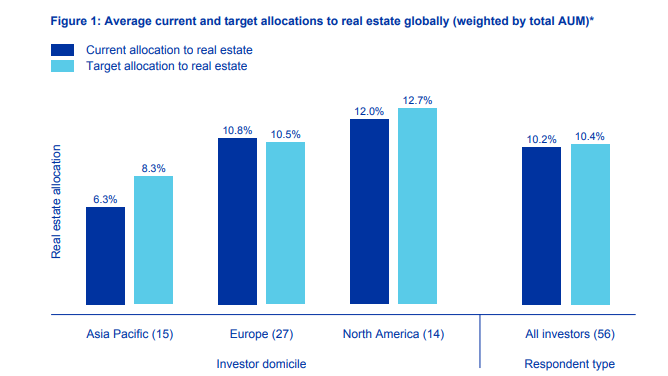

In a major change from the past few years, European investors are expected to look at decreasing their allocation to real estate in 2023, a new Investors’ Intention survey released by Inrev has revealed.

Premium subscriber content – please log in to read more or take a free trial.